Valuation of bonds and shares

The valuation of any asset, real finance is equivalent to the current value of cash flows estimated from it.

Bond:

A bond is defined as a long-term debt tool that pays the bondholder a specified amount of periodic interest over a specified period of time. In financial area, a bond is an instrument of obligation of the bond issuer to the holders. It is a debt security, under which the issuer owes the holders a debt and, depending on the terms of the bond, is obliged to pay them interest and/or to recompense the principal at a later date, called the maturity date. Interest is generally payable at fixed intervals such as semi-annual, annual, and monthly. Sometimes, the bond is negotiable, i.e. the ownership of the instrument can be relocated in the secondary market. This means that once the transfer agents at the bank medallion stamp the bond, it is highly liquid on the second market.

It can be established that Bonds signify loans extended by investors to companies and/or the government. Bonds are issued by the debtor, and acquired by the lender. The legal contract underlying the loan is called a bond indenture.

Normally, bonds are issued by public establishments, credit institutions, companies and supranational institutions in the major markets. Simple process for issuing bonds is through countersigning. When a bond issue is underwritten, one or more securities firms or banks, forming a syndicate, buy the whole issue of bonds from the issuer and re-sell them to investors. The security firm takes the risk of being unable to sell on the issue to end investors. Primary issuance is organised by book runners who arrange the bond issue, have direct contact with depositors and act as consultants to the bond issuer in terms of timing and price of the bond issue. The book runner is listed first among all underwriters participating in the issuance in the tombstone ads commonly used to announce bonds to the public. The book-runners' willingness to underwrite must be discussed prior to any decision on the terms of the bond issue as there may be limited demand for the bonds.

On the contrary, government bonds are generally issued in an auction. In some cases both members of the public and banks may bid for bonds. In other cases, only market makers may bid for bonds. The overall rate of return on the bond depends on both the terms of the bond and the price paid. The terms of the bond, such as the coupon, are fixed in advance and the price is determined by the market.

Key Features of Bonds:

- The par (or face or maturity) value is the amount repaid (excluding interest) by the borrower to the lender (bondholder) at the end of the bond's life.

- The coupon rate decides the “interest” payments. Total annual amount = coupon rate x par value.

- A bond's maturity is its remaining life, which drops over time. Original maturity is its maturity when it is issued. The firm promises to repay the par value at the end of the bond’s maturity.

- A sinking fund involves principle repayments (buying bonds) prior to the issue's maturity.

- Exchangeable bonds can be converted into a pre-specified number of shares of stock. Characteristically, these are shares of the issuer's common stock.

- The call provision permits the issuer to buy the bonds (repay the loan) prior to maturity for the call price. Calling may not be allowed in the first few years.

Bond valuation:

Valuation of a bond needs an estimate of predictable cash flows and a required rate of return specified by the investor for whom the bond is being valued. If it is being valued for the market, the markets expected rate of return is to be determined or estimated. The bond’s fair value is the present value of the promised future coupon and principal payments. At the time of issue, the coupon rate is set such that the fair value of the bonds is very close to its par value. Afterwards, as market conditions change, the fair value may differ from the par value.

At the time of issue of the bond, the interest rate and other conditions of the bond would have been impacted by numerous factors, such as current market interest rates, the length of the term and the creditworthiness of the issuer. These factors are likely to change with time, so the market price of a bond will diverge after it is issued. The market price is expressed as a percentage of nominal value. Bonds are not necessarily issued at par (100% of face value, corresponding to a price of 100), but bond prices will move towards par as they approach maturity (if the market expects the maturity payment to be made in full and on time) as this is the price the issuer will pay to redeem the bond. This is termed as "Pull to Par". At other times, prices can be above par (bond is priced at greater than 100), which is called trading at a premium, or below par (bond is priced at less than 100), which is called trading at a discount.

The market price of a bond is the present value of all expected future interest and principal payments of the bond discounted at the bond's yield to maturity, or rate of return. That relationship is the definition of the redemption yield on the bond, which is expected to be close to the current market interest rate for other bonds with similar characteristics. The yield and price of a bond are inversely related so that when market interest rates rise, bond prices fall and vice versa. The market price of a bond may be cited including the accumulated interest since the last coupon date. The price including accrued interest is known as the "full" or "dirty price". The price excluding accrued interest is known as the "flat" or "clean price".

The interest rate divided by the current price of the bond is termed as current yield. This is the nominal yield multiplied by the par value and divided by the price. There are other yield measures that exist such as the yield to first call, yield to worst, yield to first par call, yield to put, cash flow yield and yield to maturity.

The link between yield and term to maturity for otherwise identical bonds is called a yield curve. The yield curve is a graph plotting this relationship. Bond markets, dissimilar to stock or share markets, sometimes do not have a centralized exchange or trading system. Reasonably, in developed bond markets such as the U.S., Japan and Western Europe, bonds trade in decentralized, dealer-based over-the-counter markets. In such a market, market liquidity is offered by dealers and other market contributors committing risk capital to trading activity. In the bond market, when an investor buys or sells a bond, the counterparty to the trade is almost always a bank or securities firm which act as a dealer. In some cases, when a dealer buys a bond from an investor, the dealer carries the bond "in inventory", i.e. holds it for his own account. The dealer is then subject to risks of price fluctuation. In other cases, the dealer instantly resells the bond to another investor.

Bond markets can also diverge from stock markets in respect that in some markets, investors sometimes do not pay brokerage commissions to dealers with whom they buy or sell bonds. Rather, the dealers earn income through the spread, or difference, between the prices at which the dealer buys a bond from one investor the "bid" price and the price at which he or she sells the same bond to another investor the "ask" or "offer" price. The bid/offer spread signifies the total transaction cost associated with transferring a bond from one investor to another.

Share:

In financial markets, a share is described as a unit of account for different investments. It is also explained as the stock of a company, but is also used for collective investments such as mutual funds, limited partnerships, and real estate investment trusts. The phrase 'share' is delineated by section 2(46) of the Companies Act 1956 as "share means a share in the share capital of a company includes stock except where a distinction between stock and share is expressed or implied".

Companies issue shares which are accessible for sale to increase share capital. The owner of shares in the company is a shareholder (or stockholder) of the corporation. A share is an indivisible unit of capital, expressing the ownership affiliation between the company and the shareholder. The denominated value of a share is its face value, and the total of the face value of issued shares represent the capital of a company, which may not reflect the market value of those shares. The revenue generated from the ownership of shares is a dividend. The process of purchasing and selling shares often involves going through a stockbroker as a middle man.

Share valuation:

Shares valuation is done according to numerous principles in different markets, but a basic standard is that a share is worth price at which a transaction would be expected to occur to sell the shares. The liquidity of markets is a major consideration as to whether a share is able to be sold at any given time. An actual sale transaction of shares between buyer and seller is usually considered to provide the best prima facie market indicator as to the "true value" of shares at that specific time.

Shares are often promised as security for raising loans. When one company acquires majority of the shares of another company, it is required to value such shares. The survivors of deceased person who get some shares of company made by will. When shares are held by the associates mutually in a company and dissolution takes place, it is important to value the shares for proper distribution of partnership property among the partners. Shares of private companies are not listed on the stock exchange. If such shares are appraisable by the shareholders or if such shares are to be sold, the value of such shares will have to be determined. When shares are received as a gift, to determine the Gift Tax & Wealth Tax, the value of such shares will have to be ascertained.

Values of shares:

- Face Value: A Company may divide its capital into shares of @10 or @50 or @100 etc. Company’s share capital is presented as per Face Value of Shares. Face Value of Share = Share Capital / Total No of Share. This Face Value is printed on the share certificate. Share may be issued at less (or discount) or more (or premium) of face value.

- Book Value: Book value is the value of an asset according to its balance sheet account balance. For assets, the value is based on the original cost of the asset less any devaluation, amortization or impairment costs made against the asset.

- Cost Value: Cost value is represented as price on which the shares are purchased with purchase expenses such as brokerage, commission.

- Market Value: This values is signified as price on which the shares are purchased or sold. This value may be more or less or equal than face value.

- Capitalised Value:

Capitalised Value of profit

Capitalised Value of share

=

-------------------------------------Total no. of shares

- Fair Value: This value is the price of a share which agreed in an open and unrestricted market between well-informed and willing parties dealing at arm’s length who are fully informed and are not under any compulsion to transact.

- Yield Value: This value of a share is also called Capitalised value of Earning Capacity. Normal rate of return in the industry and actual or expected rate of return of the firm are taken into consideration to find out yield value of a share.

Need for Valuation:

- When two or more companies merge

- When absorption of a company takes place.

- When some shareholders do not give their approval for reconstruction of the company, there shares are valued for the purpose of acquisition.

- When shares are held by the associates jointly in a company and dissolution takes place, it becomes essential to value the shares for proper distribution of partnership property among the partners.

- When a loan is advanced on the security of shares.

- When shares of one type are converted in to shares of another type.

- When some company is taken over by the government, compensation is paid to the shareholders of such company and in such circumstances, valuation of shares is made.

- When a portion of shares is to be given by a member of proprietary company to another member, fair price of these shares has to be made by an auditor or accountant.

Methods of valuation:

1. Net Assets Value (NAV) Method: This method is called intrinsic value method or breakup value method (Naseem Ahmed, 2007). It aims to find out the possible value of share in at the time of liquidation of the company. It starts with calculation of market value of the company. Then amount pay off to debenture holders, preference shareholders, creditors and other liabilities are deducted from the realized amount of assets. The remaining amount is available for equity shareholders.

Under this method, the net value of assets of the company are divided by the number of shares to arrive at the value of each share. For the determination of net value of assets, it is necessary to estimate the worth of the assets and liabilities. The goodwill as well as non-trading assets should also be included in total assets. The following points should be considered while valuing of shares according to this method:

- Goodwill must be properly valued

- The fictitious assets such as preliminary expenses, discount on issue of shares and debentures, accumulated losses etc. should be eliminated.

- The fixed assets should be taken at their realizable value.

- Provision for bad debts, depreciation etc. must be considered.

- All unrecorded assets and liabilities (if any) should be considered.

- Floating assets should be taken at market value.

- The external liabilities such as sundry creditors, bills payable, loan, debentures etc. should be deducted from the value of assets for the determination of net value.

The net value of assets, determined so has to be divided by number of equity shares for finding out the value of share. Thus the value per share can be determined by using the following formula:

Value Per Share= (Net Assets-Preference Share Capital)/Number Of Equity Shares

Net asset method is useful in case of amalgamation, merger, acquisition, or any other form of liquidation of a company. This method determines the rights of various types of shares in an efficient manner. Since all the assets and liabilities are values properly including ambiguous and intangibles, this method creates no problem for valuation of preference or equity share. However it is difficult to make proper valuation of good will and estimate net realisation value of various other assets of the company. Such estimates are likely to be influenced by personal factors of valuers. This method is suitable in case of companies likely to be liquidated in near future or future maintainable profits cannot be estimated properly or where valuation of shares by this method is required statutorily (Naseem Ahmed, 2007).

2. Yield-Basis Method: Yield is the effective rate of return on investments which is invested by the investors. It is always expressed in terms of percentage. Since the valuation of shares is made on the basis of Yield, it is termed as Yield-Basis Method.

Yield may be calculated as under:

|

|

|

Normal profit |

|

|

|

Yield |

= |

|

X |

100 |

|

|

|

Capital Employed |

|

|

Under Yield-Basis method, valuation of shares is made on;

I. Profit Basis: Under this method, profit should be determined on the basis of past average profit; subsequently, capitalized value of profit is to be determined on the basis of normal rate of return, and, the same (capitalized value of profit) is divided by the number of shares in order to find out the value of each share.

Following procedure is adopted:

|

|

|

Profit |

|

|

|

Capitalised value of profit |

= |

|

X |

100 |

|

|

|

Normal rate of return |

|

|

|

|

|

Capitalised value of profit |

|

Value of each equity share |

= |

|

|

|

|

Number of shares |

|

Or, Value

of each equity share |

|

Profit |

|

|

|

= |

|

X |

100 |

|

|

|

Normal rate of return

X Number of equity shares |

|

|

II. Dividend Basis: In this type of valuation, shares are valued on the basis of expected dividend and normal rate of return. The value per share is calculated through following formula:

Expected rate of dividend = (profit available for dividend/paid up equity share capital) X 100

Value per share = (Expected rate of dividend/normal rate of return) X 100

Valuation of shares may be made either (a) on the basis of total amount of dividend, or (b) on the basis of percentage or rate of dividend

3. Earning Capacity (Capitalisation) Method: In this valuation procedure, the value per share is calculated on the basis of disposable profit of the company. The disposable profit is found out by deducting reserves and taxes from net profit (Naseem Ahmed, 2007). The following steps are applied for the determination of value per share under earning capacity:

Step 1: To find out the profit available for dividend

Step 2: To find out the capitalized value

Capitalized Value = (Profit available for equity dividend/Normal rate of return) X 100

Step 3: To find out value per share

Value per share = Capitalized Value/Number of Shares

In this method, profit available for equity shareholders, as calculated under capitalization method, are capitalized on the basis of normal rate of return. Then the value of equity share is ascertained by dividing the capitalized profit by number of equity share as shown under (Naseem Ahmed, 2007):

Appraisal of Earning Capacity: This method is suited only when maintainable profit and normal rate of return (NRR) can be ascertained clearly. It is possible when market information is easily available. However, while calculating NRR, risk factors must be taken into consideration (Naseem Ahmed, 2007).

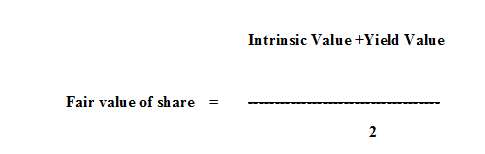

4. Average (Fair Value) Method: In order to overcome the inadequacy of any single method of valuation of shares, Fair Value Method of shares is considered as the most appropriate process. It is simply an average of intrinsic value and yield value or earning capacity method. For valuing shares of investment companies for wealth tax purposes, Fair Value Method of shares is recognized by government. It is well suited to manufacturing and other companies. The fair value can be calculated by following formula (Naseem Ahmed, 2007):

To summarize, bonds and their alternatives such as loan notes, debentures and loan stock, are IOUs issued by governments and companies in order to increase finance. They are often called fixed income or fixed interest securities, to differentiate them from equities, in that they often make known returns for the investors (the bond holders) at regular intervals. These interest payments, paid as bond coupons, are fixed, unlike dividends paid on equities, which can be variable. Most corporate bonds are redeemable after a specified period of time. Valuation of share involves the use of financial and accounting data. It depends on valuer’s judgement experience and knowledge.