What is GST bill and how it impacts on common man

Indirect Tax system is highly complicated in India because there are various types of taxes that are charged by the Central and State Governments on Goods and Services. These taxes include Entertainment Tax for watching film, Value Added Tax (VAT) for purchasing goods & services by consumer. Other taxes are excise duties, Import Duties, Luxury Tax, Central Sales Tax, Entry tax, and Service Tax.

Businessmen have to maintain accounts which need to obey with all the applicable laws.

Many experts have suggested that to resolve the issues of different types of taxes, there is a need issue to streamline all indirect taxes and implement a "single taxation" system. This system is entitled as Goods and Services Tax, abbreviated as GST. The GST will be levied both on Goods and Services.

Earlier, GST was introduced during 2007-08 budget session. On 17th December 2014, the current Union Cabinet ministry permitted the proposal for introduction GST Constitutional Amendment Bill. On 19th of December 2014, the bill was offered on GST in Loksabha. The Bill is presented in Budget session.

In simple term, GST is a tax that people need to pay on supply of goods & services. Any person, who is providing or supplying goods and services is responsible to charge GST. GST is the huge reform in indirect tax structure in Indian financial scenario since the economy originated to be opened up 25 years ago, at last looks set to become reality. The Constitution (122nd) Amendment Bill introduced in Rajya Sabha recently, on the back of a broad political agreement and heightened by the good aspirations of the Congress. Goods and Services Tax Reform was passed in Rajya Sabha and it will be set to bring in lok Sabha.

The proposed model of GST and the rate:

A dual GST system is scheduled to be implemented in India as proposed by the Empowered Committee under which the GST will be divided into two parts:

- State Goods and Services Tax (SGST)

- -Central Goods and Services Tax (CGST)

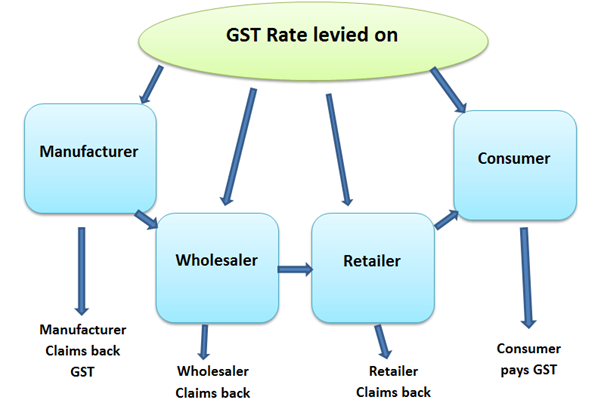

GST is a consumption based tax. It is based on the "Destination principle." Goods and Services Tax is imposed on goods and services at the place where final/actual consumption occurs. GST is accumulated on value-added goods and services at each stage of sale or buying in the supply chain. GST paid on the obtaining goods and services can be set off against that payable on the supply of goods or services. The producer or wholesaler or retailer will pay the applicable GST rate but will claim back through tax credit mechanism.

Application and tools of goods and services taxes

GST will be charged on the place of consumption of Goods and services. It can be levied on following:

- Intra-state supply and consumption of goods & services

- Inter-state movement of goods

- Import of Goods & Services

Important features of Goods and Service Tax, bill:

- The GST shall have two mechanisms: one levied by the Centre (hereinafter referred to as Central GST), and the other levied by the States (hereinafter denoted to as State GST). Rates for Central GST and State GST would be set appropriately, reflecting revenue considerations and acceptability. This twofold GST model would be implemented through manifold statutes (one for CGST and SGST statute for every State).

- Though, the basic structures of law such as chargeability, definition of taxable event and taxable person, measure of levy including valuation provisions, basis of classification would be uniform across these statutes as far as practicable.

- The Central GST and the State GST would be applicable to all transactions of goods and services made for a consideration except the exempted goods and services, goods which are outside the purview of GST and the dealings which are below the prescribed threshold limits.

- The Central GST and State GST are to be paid to the accounts of the Centre and the States independently. It must be ensured that account-heads for all services and goods would have indication whether it relates to Central GST or State GST.

- Since the Central GST and State GST are to be treated distinctly, taxes paid against the Central GST shall be permitted to be taken as input tax credit (ITC) for the Central GST and could be utilized only against the payment of Central GST.

- Cross utilization of ITC between the Central GST and the State GST would not be permitted except in the case of inter-State supply of goods and services under the IGST model.

- Preferably, the problem related to credit accumulation on account of refund of GST should be evaded by both the Centre and the States except in the cases such as exports, purchase of capital goods, input tax at higher rate than output tax where, again refund/adjustment should be completed in a time bound manner.

- In order to make it practical, uniform procedure for collection of both Central GST and State GST is recommended in the respective legislation for Central GST and State GST.

- The supervision of the Central GST to the Centre and for State GST to the States would be given. This would infer that the Centre and the States would have parallel jurisdiction for the entire value chain and for all taxpayers on the basis of thresholds for goods and services prescribed for the States and the Centre.

- The present threshold prescribed in different State VAT Acts below which VAT is not applicable varies from State to State. A uniform State GST threshold across States is required. It is considered that a threshold of gross annual turnover of Rs.10 lakh both for goods and services for all the States and Union Territories may be approved with satisfactory compensation for the States (particularly, the States in North-Eastern Region and Special Category States) where lower threshold had prevailed in the VAT regime. To respect the interest of small traders and small scale industries and to avoid dual control, the States also considered that the threshold for Central GST for goods may be kept at Rs.1.5 crore and the threshold for Central GST for services may also be appropriately high. It may be stated that even now there is a separate threshold of services (Rs. 10 lakh) and goods (Rs. 1.5 crore) in the Service Tax and CENVAT.

- The States has opinion that Composition/Compounding Scheme for the purpose of GST should have an upper ceiling on gross annual turnover and a floor tax rate with respect to gross annual turnover. Particularly, there would be a compounding cut-off at Rs. 50 lakh of gross annual turnover and a floor rate of 0.5% across the States. The scheme would also permit option for GST registration for merchants with turnover below the compounding cut-off.

- The taxpayer would need to submit periodical returns, in common format as far as possible, to both the Central GST authority and to the concerned State GST authorities.

- Each taxpayer would be allotted a PAN-linked taxpayer identification number with a total of 13/15 digits. This would bring the GST PAN-linked system in line with the predominant PAN-based system for Income tax, facilitating data exchange and taxpayer compliance.

- For the convenience of tax payer, functions such as assessment, enforcement, scrutiny and audit would be undertaken by the authority which is collecting the tax, with information sharing between the Centre and the States.

Advantages of GST bill:

- The tax structure will be lean and simple.

- The whole Indian market will be an incorporated market which may transform into lower business costs. It can simplify seamless movement of goods across states and reduce the transaction costs of businesses.

- It is beneficial for export businesses. Because it is not applied for goods/services which are exported out of India.

- It's implementation has long term benefit. The lower tax burden could translate into lower prices on goods for customers.

- The Suppliers, manufacturers, wholesalers and retailers are able to recover GST suffered on input costs as tax credits. This decreases the cost of doing business, thus enabling reasonable prices for customers.

- It can bring more transparency and better compliance.

- GST implementation can control corruption. Number of departments (tax departments) will reduce which in turn may lead to less corruption.

- More business persons will come under the tax system thus broadening the tax base. This may lead to better and more tax revenue collections.

- Companies which are under unorganized sector will come under tax area.

- The procedure of GST registration would also be made simple, thereby improving the ease of starting a business in India.

Major challenges of GST system:

Besides benefits, there are several challenges in implementing GST bill.

- To implement the bill, there has to be lot changes at administration level.

- GST, being a consumption-based tax, states with higher consumption of goods and services will have better revenues. So, the co-operation from state governments would be major factors for the effective implementation of GST.

It is assessed that since GST substitutes many flowing taxes, the common man may get benefit after implementation. But it depends on rate fixed on the GST. With the execution of GST, a consumer will pay less tax.

GST is also advantageous for companies. GST will cut the number of taxes under the current system like VAT, excise duty, service tax, sale tax, entertainment tax, luxury tax. Single tax will be applied on both Goods and Services. This will save the managerial cost for companies.

The current indirect system is so burdensome that the trucks have to stop at check posts and toll plazas for weeks to get the clearance to enter the state which considerably lessen their average distance travelled per day. With the application of the GST, the trucks need not to stop on check posts. Therefore, it will reduce the buffer stock. In this way, it will increase the operating proficiency of the companies.

It is assumed by experts that the most substantial opposing impact for consumers may arose because petroleum is excluded of the GST domain. Subsequently, the tax costs (taxes other than GST will continue) could have a flowing impact on the whole economy. According to news reports, economic adviser has mentioned that "bringing electricity and petroleum within the scope of GST could make Indian manufacturing more competitive". Additionally, certain challenges in-built in the GST structure, such as a GST levy on maximum retail price (MRP) for packaged goods and GST on barter exchanges, will trouble to the common man.

Other economic evaluators inferred that GST will eliminate flowing effect of taxes rooted in cost of production of goods and services and will provide seamless credit throughout value chain. This will considerably decrease cost of home-grown goods and will encourage ‘Make in India’. The sectors which have long value chain from basic goods to final consumption stage with operation spread in multiple states such as FMCG, pharma, consumer durables, automobiles and engineering goods will be the major recipients of GST system. It is supposed that GST will simplify business operations in India. Integration of existing multiple taxes into single GST will considerably lessen cost of tax compliance and transaction cost

To sum up facts, the GST is an indirect tax which entails that the tax is approved till the last stage where it is the purchaser of the goods and services who bears the tax. The GST will substitute most other indirect taxes and synchronize the differential tax rates on mass-produced goods and services. The government of India claims that GST will enhance Indian GDP by 2%. With the enactment of GST, customers will have funds to spend because of lower tax rates. It can be said that it will completely change the indirect tax system in India.