Infrastructure: Energy, Ports, Roads, Airports, Railways

For any country, infrastructure is important for its development as it offers basic facilities required for the smooth functioning of society. It can be said that infrastructure is the fundamental physical or organizational structures needed for the operation of a civilisation or enterprises. Speedy growth needs to be maintained by an efficient, reliable and innocuous transport system. This is particularly important for an economy concerned about competitiveness. To fulfil these increasing demands, huge investments is needed in roads, railways, ports and civil aviation sectors for increase of capacities and transformation. The public sector play vital role in building transport infrastructure. Nevertheless, the resources needed are much larger than the public sector can provide and public investment is therefore needed to be supplemented by private sector investments, in Public-Private Partnership (PPP) mode. This strategy was followed in the Eleventh Plan and has begun to display results in both the Centre and the State sectors.

Public Private Partnerships (PPPs) are progressively becoming the desired mode for construction and operation of infrastructure projects, both in developed and developing countries. Public Private Partnerships are expected to expand resource availability as well as improve efficacy of infrastructure service delivery. Time and cost swamped in construction of Public Private Partnership projects are also anticipated to be lower compared to traditional public procurement. The acceptance of standardized documents such as model concession agreements and bidding documents for award of Public Private Partnership projects have streamlined and enhanced decision-making by agencies in a manner that is fair, transparent and competitive. This approach has contributed considerably to the recent paces in rolling out a large number of Public Private Partnership projects in different sectors. According to the Private Participation in Infrastructure database of the World Bank, India is second only to China in terms of number of Public Private Partnership projects and in terms of investments, it is second to Brazil.

Since last decades, the government has faced with a huge resource crisis. The combined deficit of the central and state governments is approximately 10 per cent of GDP. Government borrowing has been covered through the Fiscal Responsibility and Budgetary Management Act. This essentially limits state participation in infrastructure financing, thus opening the door to innovative approaches, such as Public Private Partnerships. The Government of India has been encouraging private sector investment and participation in all infrastructure sectors. As the National Development Council has made clear, ‘Increased private participation has now become a requirement to mobilise the resources needed for infrastructure expansion and upgrading’. The Public Private Partnership model has been fairly successful in many advanced countries and it is a robust model. PPPs in India are in a nascent stage, but are gaining approval and support given the dire need to improve infrastructure in the country. An appraisal of international best practice in PPPs suggests numerous issues that public authorities must address when considering their use for procuring public infrastructure projects. These include:

- Whether PPP arrangements will result in better value for money than conventional procurement methods.

- Whether the project is affordable in the long term, given overall budgetary constraints.

- How willing is the private sector to be involved in the provision of public services.

- What type of PPP arrangement is most appropriate for a particular project.

Presently, the PPP model in India has been slightly successful with numerous projects being implemented across sectors. However, one of the main problems confronting infrastructure and PPPs in India is the delay in implementing and executing large-scale projects resulting in time and cost overruns. Efficiency in implementing infrastructure projects in India is a rarity. The PPP model is a multifaceted and leading to problems at various stages of implementation and execution of the project. PPP model has many problems such as these are poorly drafted contracts, Contract manager assigned insufficient resources. There is lack of experience in either the public sector or the provider teams, a failure to adopt an attitude towards partnership. It is found that there are personality clashes between project team personnel, lack of understanding of the complexity, context, and dependencies of the contract, unclear identification of authority and responsibility in relation to commercial decisions, lack of measurement of performance, focus on existing arrangements rather than emphasis on potential improvements, and inadequate monitoring and management of statutory, political, and commercial risks.

Major PPPs models in India are as under:

- Delhi, Mumbai, Hyderabad and Bengaluru airports.

- Ultra-mega power projects at Sasan (Madhya Pradesh), Mudra (Gujarat), Krishnapatnam (Andhra Pradesh), and Tilaiya ( Jharkhand).

- Container terminals at Mumbai, Chennai.

- Tuticorin ports.

- 15 concessions for operations of container trains.

- Jhajjar power transmission project in Haryana.

- 298 national and state highway projects.

Table: PPP Projects in Central and State Sectors in India (Source: Planning Commission and Infrastructure.gov.in)

|

Name of Infrastructure |

No. of

projects |

Project cost

(INR in Cr.) |

|

National Highways |

172 |

96,152 |

|

Major ports |

21 |

14,735 |

|

Airports |

5 |

19,111 |

|

Railways |

7 |

2,418 |

|

Energy |

4 |

17,500 |

|

Total |

209 |

149,916 |

|

State sector |

||

|

Roads |

273 |

123,386 |

|

Ports |

41 |

66,479 |

|

Airports |

- |

- |

|

Railways |

2 |

1,494 |

|

Urban infrastructure |

166 |

84,914 |

|

Energy

|

65 |

56,185 |

|

Tourism |

50 |

4,497 |

|

Other Sectors |

34 |

3,756 |

|

Total |

631 |

340,711 |

Table: India PPP Projects in India (Source: Planning Commission)

|

Sector |

Number |

|

Airport |

5 |

|

Education |

19 |

|

Health care |

8 |

|

Energy |

72 |

|

Ports |

62 |

|

Roads |

445 |

|

Railways |

9 |

|

Tourism |

53 |

|

Urban development |

167 |

|

Total Projects |

840 |

Transport is the leading Public Private Partnerships sector in India both by number of projects and investments, mostly due to the huge number of road sector projects. Additionally, efforts are needed to mainstream Public Private Partnerships in several areas such as power transmission and distribution, water supply and sewerage and railways where there is substantial resource deficit and also a need for efficient delivery of services. Similar efforts would also need to be commenced in social sectors, especially health and education.

1. Energy: Energy represents as one of the most important bond for viable economic growth and human development. The per capita energy consumption is one of the major parameters used to assess the stage of economic and social development of any country. It is recognized by professionals that energy is one of the major drivers of a mounting economy for developing country such as India and it is an essential building block of economic progress. To cater the demands of a developing nation, the Indian energy sector has observed a rapid growth. Many areas such as the resource exploration and exploitation, capacity additions, and energy sector reforms have been transformed. Though, resource augmentation and growth in energy supply have failed to meet the ever increasing demands exerted by the multiplying population, rapid urbanization and progressing economy. Hence, serious energy scarcities continue to spate India and compel it to rely on imports.

The growth of energy sector is a relationship of multifaceted factors that include policies and regulations, political and economic stability, resources endowment, technology development and adoption, large capital investments on long maturation period projects, complex risk profiles, supporting goods and services sector, skilled and managerial manpower and various commercial and contractual aspects. In order to reach energy to the end users, it is necessary that there must be development of huge supporting infrastructure covering railways and roadways, transmission and distribution grids, transmission and distribution pipelines, storages, marketing facilities among others. Progression of energy sector also leads to extraction of natural resources and therefore responsibilities for environment management and social aspects needs to be addressed. India is set to remain one of the top five energy consuming country as it continues with its economic growth programs, and strive to improve its standard of living.

According to IEA, India has fourth rank in energy consumption with over 4% of the world's total annual energy consumption and expected to be the third largest energy consumer by 2025 after USA and China with favourable economic and social developments. The Twelfth Five Year Plan put special emphasis on development of the infrastructure sector including energy, as the availability of quality infrastructure is important not only for sustaining high growth but also ensuring that the growth is inclusive.

With reference to energy Infrastructure in India, It has a big energy sector which is growing speedily. India is practically well endowed with primary and renewable energy resources. In future, there will be huge investment in the energy sectors along the entire value chains and this will be led by public and private spending. Information and data on Indian energy sector is extensively available from large number of agencies. However India does not have any one agency such as EIA USA, to issue comprehensive and authentic data on the sector.

India is affluent with both exhaustible and renewable energy resources. Coal, oil, and natural gas are the three primary commercial energy sources. India’s energy strategy, till the end of the 1980s, was mainly based on availability of original resources. Coal was the largest source of energy. India is, however, poorly capable of oil assets and has to depend on crude imports to meet a major share of its needs (around 70 percent). India’s primary energy mix has been changing over a period of time.

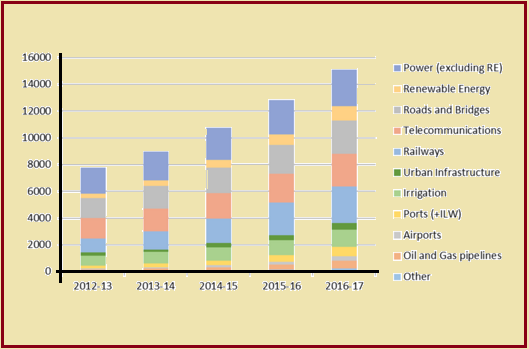

Infrastructure investment planned during 2012-2017

Even though, there is increased dependency on commercial fuels, ample quantum of energy requirements (40% of total energy requirement), especially in the rural household sector, is met by non-commercial and traditional energy sources, which include fuel wood, crop residue, biomass and animal waste, including human and draught animal power. Other forms of commercial energy of a much higher quality and efficiency are steadily replacing the traditional energy resources being consumed in the rural sector.

Coal is the most abundant fossil fuel in India and accounts for 55% of India's energy need. India's industrial heritage was built upon indigenous coal, largely mined in the eastern and the central regions of the country. Reports indicated that thirty per cent of commercial energy requirements are met by petroleum products, approximately 7.5 per cent by natural gas and 3.5 per cent by primary electricity. Resource expansion and growth in energy supply has not kept pace with growing demand and, therefore, India continues to face serious energy shortages. This has led to increased reliance on imports to meet the energy demand. Though various policy initiatives are adopted to diversify the fuel mix but considering the limited reserve potentiality of petroleum & natural gas, eco-conservation restriction on hydel project and geo-political perception of nuclear power could not suffice. It is clear that coal will continue to occupy centre-stage of India's energy scenario. Indian coal offers a fuel source to domestic energy market for the next century & beyond. Based on estimates, the consumption of coal is predicted to rise by nearly 40 percent over the next five years and almost to double by 2020.

Power Sector: Another energy source is power. Power is one of the most critical components of infrastructure vital for the economic development and wellbeing of nations. The existence and development of passable infrastructure is essential for sustained growth of the Indian economy. It is found in reports that access to affordable and reliable electricity is critical to a country’s growth and affluence. India has made substantial progress towards the expansion of its power infrastructure. It is well documented that the installed power capacity has increased from only 1713 MW (megawatts) as on 31 December 1950 to 118419 MW as on March 2005. The all India gross electricity generation, excluding that from the captive generating plants, was 5107 GWh (gigawatt-hours) in 1950 and increased to 565 102 GWh in 2003/ 04. Energy requirement increased from 390 BkWh (billion kilowatt-hours) during 1995/ 96 to 591 BkWh (energy) by the year 2004 /05, and peak demand increased from 61 GW (gigawatts) to 88 GW over the same time period. India experienced energy shortage. Though, the growth in electricity consumption over the past decade has been slower than the GDP’s growth, this increase could be due to high growth of the service sector and efficient use of electricity.

Key investments in the Indian power sector are as under (power sector report, January, 2016):

- World's largest renewable energy company, plans to continue its focus on ‘Make in India’ by further reducing the cost of renewable energy and developing over 15 gigawatts (GW) of wind and solar projects in the country by 2022.

- ThyssenKrupp India, the Indian arm of the German engineering conglomerate, plans to make high-grade environment-friendly boilers which use less fuel, for the Indian power sector by collaborating with a foreign company.

- Aditya Birla Group has announced a partnership with the Abraaj Group, a leading investor in global growth markets, to build a large-scale renewable energy platform that will develop utility-scale solar power plants in India.

- Sterlite Grid, India’s largest private operator of transmission systems is joining hands with US major - Burn & McDonnell for its Rs 3,000-crore (US$ 462.5 million) power transmission project in the Kashmir valley.

- Inox Wind Ltd, a subsidiary of Gujarat Fluorochemicals, a wind energy solutions provider, plans to double its manufacturing capacity to 1,600 MW at a total investment of Rs 200 crore (US$ 31.6 million) by the end of the next financial year.

- The Dilip Shanghvi family, founders of Sun Pharma, acquired 23 per cent stake in Suzlon Energy, with a preferential issue of fresh equity for Rs 1,800 crore (US$ 284.8 million).

- Reliance Power Ltd signed an accord with the Government of Rajasthan for developing 6,000 MW of solar power projects in the state over the next 10 years.

- Hilliard Energy plans to invest Rs 3,600 crore (US$ 600 million) in Ananthapur district of Andhra Pradesh in the solar and wind power sector for the generation of 650 MW of power.

- Solar technology provider SunEdison signed a definitive agreement to acquire Continuum Wind Energy, Singapore, with assets in India. The company, headquartered in Belmont, California, would take over 242 MW of operating wind assets that Continuum owns and operates in Maharashtra and Gujarat as well as 170 MW of assets under construction.

- Japanese internet and telecommunications giant SoftBank, along with Bharti Enterprises (of Sunil Mittal) and Taiwanese manufacturing giant Foxconn, plan to invest US$ 20 billion in solar energy projects in India.

Major initiatives taken by the Government of India to improve the Indian power sector are as under (power sector report, January, 2016):

- The Union Cabinet has approved the Ujwal DISCOM Assurance Yojna(UDAY) for financial turnaround and revival of power distribution companies (DISCOMs), which will ensure accessible, affordable and available power for all.

- The Government of India has resolved the issues regarding transfer of mining leases and grant of forest clearances to the winning bidders of coal blocks. It expects operations to start in about 10 more mines by March 2016, easing coal availability to the projects attached to these mines.

- The Ministry of Power has planned to provide electricity to 18,500 villages in three years under the Deendayal Upadhyaya Gram Jyoti Yojana (DUGJY). Out of these, 3,500 villages would receive electricity through off-grid or renewable energy solutions.

- The Ministry of New & Renewable Energy is implementing two national level programmes, namely Grid Connected Rooftop & Small Solar Power Plants Programme and Off-Grid & Decentralised Solar Applications, in order to promote installation of solar rooftop systems, as per Mr Piyush Goyal, Minister of State (Independent Charge) for Power, Coal & New and Renewable Energy.

- The Government of Odisha plans to set up a large 1,000-MW solar power park under public-private partnership (PPP) mode involving an investment of about Rs 6,500 crore (US$ 1 billion).

- The Government of Telangana plans to set up an incubator centre, in collaboration with University of Austin, Texas, for start-ups in the renewable energy sector, to support new companies entering the renewable energy market.

- A Joint Indo-US PACE Setter Fund has been established, with a contribution of US$ 4 million from each side to enhance clean energy cooperation.

- The Government of India announced a massive renewable power production target of 175,000 MW by 2022; this comprises generation of 100,000 MW from solar power, 60,000 MW from wind energy, 10,000 MW from biomass, and 5,000 MW from small hydro power projects.

- The Union Cabinet of India approved 15,000 MW of grid-connected solar power projects of National Thermal Power Corp Ltd (NTPC).

- The Indian Railways signed a bilateral power procurement agreement with the Damodar Valley Corporation (DVC). The agreement was signed between North Central Railway and DVC. This is the first time the Railways will directly buy power from a supplier.

- US Federal Agencies committed a total of US$ 4 billion for projects and equipment sourcing, one of the biggest deals for the growing renewable energy sector in India.

Oil and Natural Gas:

India's consumption of natural gas has increased at rapid rate than any other fuel in the recent years. Industries such as power generation, fertilizer, and petrochemical production are shifting towards natural gas. India's natural gas consumption has been met completely through domestic production in the past. However, in the last 4-5 years, there has been a huge unmet demand of natural gas in India, mainly required for the core sectors of the economy. To bridge this gap, apart from encouraging domestic production, the import of LNG (liquefied natural gas) is being considered as viable solutions for India’s expected gas shortages. Several LNG terminals have been planned in the country.

Two LNG terminals have already been commissioned:

- Petronet LNG Terminal of 5 MTPA (million tonnes per annum) at Dahej.

- LNG import terminal at Hazira.

Renewable Energy Sources:

Renewable energy sources offer feasible opportunity to address the energy security concerns of a country. Currently, India has one of the highest potentials for the effective use of renewable energy. India is the world’s fifth major producer of wind power after Denmark, Germany, Spain, and the USA. There is a substantial potential in India for generation of power from renewable energy sources such as wind, small hydro, biomass, and solar energy. The country has an assessed SHP (small-hydro power) potential of about 15000 MW. Installed combined electricity generation capacity of hydro and wind has increased from 19194 MW in 1991/ 92 to 31995 MW in 2003/ 04, with a compound growth rate of 4.35% during this period. Other renewable energy technologies include solar photovoltaic, solar thermal, small hydro, and biomass power are also spreading. Efficient use of renewable energy sources offers enormous economic, social, and environmental benefits. The potential for power production from captive and field-based biomass resources, using technologies for distributed power generation, is assessed at 19500 MW including 3500 MW of exportable surplus power from bagasse-based cogeneration in sugar mills.

The Twelfth Five Year Plan puts special emphasis on development of the infrastructure sector including energy, as the availability of quality infrastructure is important not only for supporting high growth but also ensuring that the growth is inclusive.

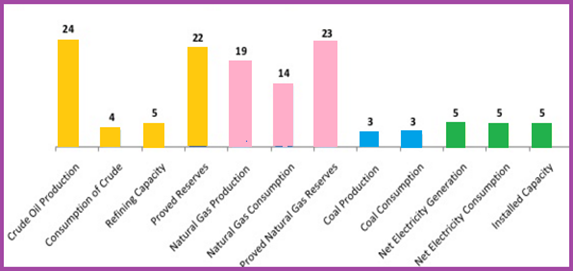

India's global ranking, major energy parameters

Unbundling of infrastructure projects, public private partnerships (PPP), and more transparent regulatory mechanisms have encouraged private investors to upsurge their participation in infrastructure sectors. Their share in infrastructure investment increased from 22 per cent in the Tenth Five Year Plan to 38 per cent in the Eleventh Plan and is expected to be about 48 per cent during the Twelfth Five Year Plan. Yet, more than half of the resources required for infrastructure would need to come from the public sector, from the government. This would require not only the formation of the fiscal space but also use of a rational pricing policy. Additionally, scaling up private-sector participation on a sustainable basis will require to redefine the delineations of their participation for the growth of infrastructure sector in a clear and objective manner with a comprehensive regulatory mechanism in place.

With reference to energy sector, during the Eleventh Five Year Plan, nearly 55,000 MW of new generation capacity was created but still there is deficit. Reports designated that resources allocated to energy supply are not adequate to narrow the gap between energy needs and energy availability. The potential for energy generation depends upon the country's natural resource endowments and the technology to harness them. India has both non-renewable reserves (coal, lignite, petroleum, and natural gas) and renewable energy sources (hydro, wind, solar, biomass, and cogeneration bagasse). The projected reserves of non-renewable and the potential from renewable energy resources change with the research and development of new reserves and the pace of their investigation.

Growth of core industries and infrastructure services (in per cent) (Source: Ministry of Statistics and Programme Implementation (MOSPI) and O/o The Economic Adviser, DIPP)

|

Sl No. |

Sector |

Unit |

2009-10 |

2010-11 |

2011-12 |

2011 |

2012 (April-Dec) |

|

1 |

Power |

Bill unit |

6.8 |

5.7 |

8.1 |

9.3 |

4.6 |

|

2 |

Coal |

MT |

8 |

0 |

1.3 |

-2.7 |

5.7 |

|

3 |

Finished steel |

MT |

3.2 |

9.6 |

8.5 |

9.1 |

3.6 |

|

4 |

Fertilizers |

MT |

13.2 |

1 |

-0.1 |

-0.5 |

-3.4 |

|

5 |

Cement |

MT |

10.1 |

4.3 |

6.4 |

5.8 |

6.1 |

|

6 |

Petroleum:

a)

Crude oil

b)

Refinery

c)

Natural gas |

MT MT MT |

0.5 -0.4 44.8 |

11.9 3 9.9 |

1 3.2 -8.9 |

1.9 4 -8.8 |

-0.4 6.9 -13.3 |

|

7 |

Railway revenue earning freight

traffic |

MT |

6.6 |

3.8 |

5.2 |

4.2 |

4.7 |

|

8 |

Cargo handling at major ports |

MT |

5.7 |

1.6 |

-1.7 |

1.3 |

-2.9 |

|

9 |

Civil Aviation:

a)

Export cargo handled

b)

Import cargo handled

c)

Passengers handled at

international terminals

d)

Passengers handled at domestic

terminals |

Tonnes Tonnes Lacs Lacs |

10.4 7.9 5.7 14.5 |

13.4 20.6 11.5 16.1 |

-2.2 -1.6 7.6 15 |

-1.3 1.8 7.5 18.5 |

-1.0 -9.7 2.8 -5.5 |

|

10 |

Telecommunications; Cell phone connections |

Thousand lines |

47.3 |

18 |

-52.7 |

-49.6 |

- |

|

11 |

Roads: Upgradation of highways

i)

NHAI

ii)

NH(O) & BRDB |

Kms Kms |

30.9 17.3 |

21.4 4 |

-33.3 6.8 |

2.9 -32.4 |

17.3 -2.8 |

The trend in production of the key sources of conventional energy such as coal, lignite, crude petroleum, natural gas, and electricity demonstrates that in last four decades, i.e. from 1970-71 to 2010-11, the compound annual growth rate (CAGR) of production of coal, lignite, crude petroleum, natural gas, and electricity (hydro and nuclear) generation was 5.0 per cent, 6.1 per cent, 4.3 per cent, 9.1 per cent, and 4.0 per cent correspondingly.

2. Ports: Ports have crucial role in facilitating India’s international trade and also in producing economic activity in their surroundings and hinterland. India’s coastline of 7,517 km. is added with 12 major ports and 187 non-major ports. India’s ports has big challenge to increase connectivity with inland transport networks currently, which have seen considerable swells in the amount of goods transported. Traffic is projected to reach 877 million tonnes by 2011-12, and containerised cargo is expected to grow at 15.5% (CAGR) over the next 7 years. India’s present ports infrastructure is not adequate to handle the increased loads, cargo unloading at many ports is currently insufficient, even where ports have already been modernised. In addition to improving road and rail connections, projects related to port development (construction of jetties, berths, container terminals, deepening of channels to improve draft, etc.), will provide major opportunities.

The major ports are situated at Calcutta/ Haldia, Chennai, Cochin, Ennore, Jawaharlal Nehru Port at Nhava Sheva, Kandla, Mormugao, Mumbai, New Mangalore, Paradip, Tuticorin and Vishakhapatnam.

The 12 major Indian ports, which are managed by the Port Trust of India under Central Government jurisdiction, handle 90 percent of the all-India port throughput, and thus bear the brunt of sea borne trade. The 139 minor ports are under the jurisdiction of the respective State Governments. Dry and liquid bulk make up about 80 percent of the port traffic in volume with general cargo, including the containerised cargo, constituting the remaining traffic.

Map: major and intermediate ports of India

Although the bulk of Indian trade is carried by sea routes, the existing port infrastructure is unsatisfactory to handle trade flows successfully. Reports indicated that the current capacity at major ports is overstretched. The major ports together have a capacity of 215 million metric tonnes (MMT) at 1997- 98 levels. During 2001- 2002, the total cargo handled at major ports was 287.56 million tonnes as against 281.10 million tonnes during 2000- 2001. The traffic for total ports in India was worth 740.3 million tons (MT) in 2009 and this rose to 1,373.1 MT in 2015.

The Indian ports sector is dignified for significant growth driven by new manufacturing and power projects and higher cargo traffic at ports. Upsurge in containerized trade joined with the Government’s active initiatives to develop the Indian ports sector, is expected to further increase the growth. The commissioning of power projects based on imported coal and the setting up of steel projects and offshore exploration and production projects are likely to drive the Indian ports sector.

The situation of limited capacity and high demand has unavoidably resulted in port overcrowding. This results in overstrained berths leading to pre-berthing delays and longer ship turnaround time. Recently, major investments in port construction have centred on container as well as bulk facilities. Modern equipment exists for container and bulk handling. The equipment- mix for handling general cargo has to be planned and provided in a manner that suits the needs of each port. Though, several major ports lack sufficient draft for large crude tankers. Large vessels are docked at Colombo, Singapore, or Dubai, and cargo is transported to India later in smaller vessels, thereby escalating the freight cost. Furthermore, all important ports such as Mumbai, Jawaharlal Nehru Port Trust (JNPT), Visakhapatnam, and Mormugao handle more cargo than their designed capacities, further contributing to congestion and resulting in a longer turnaround time. Weak hinterland connectivity is a challenge for most Indian ports, reducing accessibility. Though private sector is involved that are encouraging the transformation and development of ports, infrastructure continues to be a major issue.

The Indian Government prioritized the development and modernization of ports as part of its five-year plan initiatives in 2007. It has been instrumental in redefining the role of ports from mere trade gateways to integral parts of the global and logistics chain. The Committee of Infrastructure constituted a Committee of Secretaries to recommend time-bound identification and complete connectivity projects to effectively address issues regarding port connectivity. Several projects are proceeding for the deepening of drafts at major ports as a part of the national maritime development program.

Although the ports in India have shown substantial improvement over years, benchmarking them against the ports in Hong Kong, Los Angeles, and Rotterdam reveals that there needs to be noticeable improvement in many factors to match with international standards.

It is observed that the performance of Indian ports does not compare favourably with that of efficient international ports. There are three important parameters such as capacity, productivity and efficiency. Indian ports lack in comparison to some of the major international ports. In international terms, labour and equipment productivity levels are still very low due to the outdated equipment, poor training, low equipment handling levels by labour, uneconomic labour practices, idle time at berth, time loss at shift change and high mining scales and low datum. In India, the government has been encouraging public-private participation in the ports sector on a build-operate-transfer (BOT) basis, thereby stepping-up capacities and traffic handling at ports, besides improving their efficiency.

To handle the increase in the sea-borne traffic on account of increase in foreign and coastal trade, major growth is required in the port infrastructure sector in the country and this will need mobilisation of significant resources. Therefore, the opening up of the port sector for privatisation is required. It is predictable that privatisation would also increase the efficiency, productivity and quality of services and also bring competitiveness in port services. It is also anticipated that the private sector participation would help to implement advanced technology and improve management techniques. Many experts realized that it is necessary to encourage the private sector participation to improve port capabilities and also in modernisation of port equipment. It is appraised that the port sector is going with substantial business hopefulness with respect to generation of increasing cargo traffic volumes and of trade in general in future.

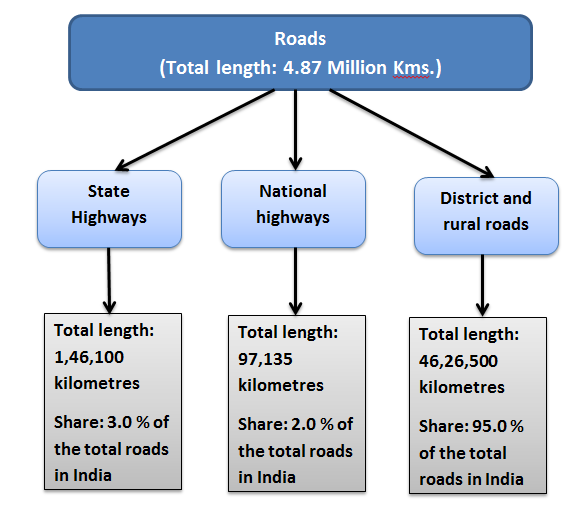

3. Roads: According to reports, India has the second largest road network in the world but most of the roads are not constructed well. These are of poor quality. Half the network is not cemented and the National Highways account for only 2.0 per cent of the total length. A start was made at giving a push to investment in roads in the Eleventh Plan. The National Highways Development Programme (NHDP)-I (Golden Quadrilateral) and NHDP-II (North-South East West links) were started before the Eleventh Plan, but were efficiently built in the Eleventh Plan. Small portions remain to be completed and these will be completed in the Twelfth Plan. The more heavily trafficked part of this network has to be supported through conversion to six-lane roads. This programme, called NHDP-VI has commenced and will be progressively expanded.

In order to guarantee the inter-connectivity of districts, work in various phases of NHDP-III, IV, V will be progressively expanded. Additionally, a new programme for construction of roads in the North East was begun in the Eleventh Plan, including the proposed Trans-Arunachal Highway. The completion of this network in the North East, along with road connectivity to Myanmar and Bangladesh will help open up this route to jointly beneficial economic cooperation with Southeast Asia. India's road network comprises of Expressways, National Highways, State Highways, Major District Roads, Other District Roads and Village Roads.

The Indian Government has also acknowledged existing infrastructure gaps and capacity constraints in the rail system, and as a consequence plans large scale investment over the five years from FY07-FY12. The Dedicated Freight Corridor project is designed to lessen congestion on the rail routes between Delhi and Mumbai and Delhi and Kolkota by building long-distance, cargo-only rail lines, at an estimated cost of US$6 billion-7 billion. Other proposed initiatives include the development of manufacturing plants for rolling stock with long-term committed procurement for several years, and the setting up of logistics parks. City metro systems are also in the pipeline. The first corridor of the Mumbai Metro Project has already been awarded to Reliance Infrastructure and the Government has asked the final shortlisted companies to submit detailed financial bids for the second phase of the Mumbai Metro.

Road infrastructure in India (Source: Ministry of road transport and highway, Techsci research July, 2015)

Major part of the existing NH consists of single-lane roads, which are ignored for long time. Their length is about 20,000 km, which could increase further during the Twelfth Plan on account of expansion of the NH network. These single lane national highways would have to be upgraded and improved to two lane standards. Since most of these roads have low density traffic, they may not be feasible on Public Private Partnership basis. Experience also recommends that annuity based projects are comparatively expensive, while conventional contacts are prone to time and cost overruns. The Ministry of Road Transport and Highways is, approving the EPC (turnkey) mode of construction. A programme for upgradation of 20,000 km to two-lane standards for EPC basis could therefore, be taken for which resources would have to be mobilised through toll revenues, market borrowings and additional budgetary support.

Besides the development of the National Highway network, it is indispensable to develop State Highways and District roads to ensure full connectivity. States must identify that good quality roads are crucial for the competitiveness of investment in the state.

The resources needed for road development will have to be mobilised by the Centre and the States for their respective spheres. It was stated that the Public Private Partnership model has been broadly used in the road sector in both the Centre and the States.

In infrastructure development of country, roads are effectual promoter of economy. 'Pradhan Mantri Gram Sadak Yojana (PMGSY), has benefited to rural households because of better connectivity to markets and also easier access to health and educational facilities.

All rural residences with a population of more than 1,000 in plain. Even after a decade, a large number of villages and habitations in rural areas remain separate due to lack of good quality roads. Rural connectivity is necessary for universalisation. Specifically, in hilly areas, Left Wing Extremist affected areas and other sparsely populated tribal areas, habitations with population up to 100 would need to be connected. This will further spread the benefits of PMGSY and promote inclusiveness.

There are revolutionary transformation made in roads of India. Yamuna Expressway is 165 km long India’s longest six-lane controlled-access expressway stretch connecting Greater Noida with Agra. Expressway is equipped with SOS booths along the route, toll free helpline ,CCTV cameras, mobile radars and one highway patrol every 25 km.

Another giant road infrastructure in India is the controlled-access freeway is 16.8 km long Eastern Freeway comprising of three segments, one of the twin tunnels, 13 km elevated road and Ghatkopar- Mankhurd Link Road. Eastern Freeway reduce travel time between South Mumbai and the Eastern Suburbs and ranked as one of the Exceptional Infrastructure Projects of the Country.

Other innovative infrastructure in India is The Kathipara cloverleaf interchanges, the largest cloverleaf flyover in the whole of Asia, sited at Alandur at the intersection and an important road junction in Chennai.

In road infrastructure, there is a serious problem of lack of maintenance of roads in India. Provision for maintenance of the National Highways comes from the non-Plan budget and typically only one-third the required amount has been provided. The introduction of toll roads on a BOT basis has helped ensure maintenance. However, the rest of the National Road Network needs maintenance and this should not suffer for want of funds. Maintenance of PMGSY is taken care of under contractual agreement. The contractors are required to maintain the roads for five years after completion. However, the State Governments are expected to provide funding. The involvement of panchayats and other PRI agencies to guarantee the maintenance of roads may be a desirable initiative. These and other alternative mechanisms will be discovered to support maintenance arrangements for the road system.

4. Airport:

Civil Aviation is the fastest rising sector of India’s transport infrastructure and it plays important role to provide enhanced connectivity. The projections for both passenger and cargo traffic growth, joined with the deficient and lagging airport & allied Infrastructure, calls for vital need to build and increase India’s Aviation Infrastructure. Since over a decade, the airport traffic in India has increased by more than 4 times and it is expected that in coming years (by 2020) to increase by traffic will increase up to 3 times. Presently, India is the 9th largest civil aviation market in the world as per reports.

Therefore it is need to device policies to modernize airport infrastructures of India that provide aviation services and passenger/cargo facilities of international standards, in a safe and secure environment. The Aviation environment in India needs to ensure the healthy growth of Airlines, together with the Airport operators and allied service providers; while also building the avionics and aviation equipment capabilities of Indian industry. The government and the statutory authorities have major role to accomplish this giant objective.

The Indian civil aviation sector is representing an unexpected growth rate since many years. In 2005-06, the passenger traffic increased by 25-30% and continually growing by 25% year-on-year. However, such a pace of growth in air traffic put strain on the aviation infrastructure, which is already stretched resulting in traffic congestions and delays at majority of the airports. At Delhi airport, approximately 327 domestic aircrafts land and take-off every day. This indicates that about 10.04 million passengers are ferried by the domestic airlines alone every year, while the terminal can handle only a meagre 7.15 million. Therefore, if a high growth in civil aviation sector is to be sustained, it would call for improvement of infrastructure facilities on several fronts.

It is projected that by 2020, Indian airports are estimated to handle;

- 100 million passengers

- Including 60 million domestic passengers

- Cargo in the range of 3.4 million tonnes per annum

After a period of havoc, the civil aviation sector showed some signs of revitalisation. Passenger traffic revived in 2013-14 with a 6 per cent year-on-year growth, after a fall in 2012-13. New terminals were also operationalised at metro airports, while new airlines began commercial operations.

The government India has taken numerous measures to improve the airport infrastructure for the country. It has envisioned a modernization plan with a view to modernize 37 non-metro airports. On the lines of the successful model of the Central Road fund, the government is considering setting up the Essential Air Service Fund to support the country’s airport infrastructure. It is viewed that there is huge requirement of funds for the development of airport infrastructure and the financial constraints coupled with other conflicting budgetary priorities of the government. The government has invited private participation in the modernization program of the major airports. Delhi and Mumbai airport development projects are being undertaken through public private partnership ventures.

There needs to be an effort towards best utilization of the existing airports through evaluating the problems of outmoded infrastructure, insufficient ground handling systems and night landing facilities, and poor passenger amenities. On the contrary, it will also be required to create new airports at several places where there is a scope. There needs to be improvement in the airside infrastructure & terminal infrastructure at India’s airports.

With rapid increase in traffic for both passenger and cargo aviation services in India, the government has put in place a program for directing investments in the Airport infrastructure through both internal resource mobilization, as well as through private sector participation in modernizing specific Airports. The Committee on Infrastructure has introduced several policy measures that would build international level airport infrastructure in India. A Model Concession Agreement is also being developed for standardizing and simplifying the PPP transactions for airports. For future projects for development of existing airports, it has been decided that the length of the runway would be at least 7,500 feet (which is needed for the A 320 and similar aircraft).

Several non-metro airports are being developed partly through the PPP model. Airports Authority of India (AAI) is developing the airside amenities and terminal buildings of these airports while city side development works are carried out on private partnership basis.

The new Greenfield airport at Hyderabad International Airport developed through PPP is functional from March 2008 and in the same way the Bangalore International airport is operated from May 23, 2008. Innovation and expansion of the Delhi and Mumbai airports are done. Chennai and Kolkata airports are also modernized. In order to ensure balanced airport development around the country, a comprehensive plan for the development of 35 non-metro airports is prepared to modernisation of airport infrastructure.

With the completion of construction of Hyderabad and, Bangalore airports and work in progress at, Delhi and Mumbai International airports, L&T is one of the Largest Airport Builder in this part of the world for Design & Construction of aviation infrastructure.

Bangalore International Airport Limited (BIAL) is State-of-the-art terminal building having an area of around 1.00 million sq. ft. It is a Construction of a 4 km runway and other infrastructure. The airport can cater to the projected traffic demand of 11.5 million passengers and handling 3 lakh tons of cargo per annum. It is modular construction adopted to ensure smooth and unified expansion to cater to future growth. There is combined Cargo handling facilities with of a total built up area of 6.00 lakhs sqft.

GMR Hyderabad International Airport Limited (GHIAL): L&T built the Greenfield International airport at Shamshabad involving terminal building and other airside works including taxiways, runways. The airport is functional and is designed to handle 12 million passengers per annum.

Main features of this infrastructure include:

- The seven level Passenger Terminal Building with an area of 1.17 million sq.ft.

- Airside works involved construction of 4.26 km long runway including developing many other infrastructures.

Delhi International Airport Private Limited (DIAL): L&T has executed the design and construction of terminal building, runway and associated works of Delhi International Airport.

Key features of this infrastructure include:

- The Passenger Terminal Building (T3) can cater to both domestic and international traffic and can handle 25 million passengers per annum, more than twice the present traffic. The total built-up area of the new terminal building (T3) is 5.2 million sq.ft..

- A new code F runway, at 4.43 km, to be one of the longest in Asia and equipped with CAT IIIB –a landing system.

- All airport facilities like baggage handling systems, IT, communication, passenger boarding bridges, flight information and displays.

The other major policy announcements made earlier in the year included the opening of global routes, extending visas-on-arrival and e-visa facilities at nine airports, allowing external commercial borrowings for maintenance, repair and overhaul facilities.

Indira Gandhi International Airport is the busiest airport in India and the new Terminal 3. It became India’s and South Asia’s largest aviation hub. The IGIA was ranked the second best airport in the world and India’s best International Airport.

However, some of the critical policy issues such as a reduction in taxes on aviation turbine fuel, airport charges, and coordinated clearances are not addressed. Meanwhile, new capacities were added by developers at key airports. New terminals were commissioned at Bengaluru and Mumbai, which together added a capacity of more than 19 million passengers per annum. The AAI also operationalised integrated terminal buildings at Ranchi, Raipur, Bhubaneswar and Goa. The government has taken initiatives to improve regional connectivity by planning no-frills airports in Tier II and Tier III cities. The design and location for five no-frills airports have been finalised.

In modernizing airports, government is taking extra care for the safety and security aspects of airports. After the Federal Aviation Administration downgraded Indian aviation to Category 2 under its International Aviation Safety Assessment Programme, the DGCA released the Standards of Services, listing the services and transactions offered by the authority. Additionally, the sustainability of airport projects is being focused on, with developers investing in greener designs and energy efficiency. Airports are also progressively investing in advanced technologies for integration and automation airports to optimise operations.

5. Railways:

Railways are another important sector that contributes for the economy of country. It is vital part of any transport network especially for freight movement. These are much more energy efficient than road transport, with a much smaller carbon footprint. Indian Railways are one of the largest railways network in the world that carry 22 million passengers every day and carry 923 million tonnes of freight a year. The railway network is also idyllic for long-distance travel and movement of bulk commodities, apart from being an energy efficient and economic mode of conveyance and transport. The Government of India has focused on investing on railway infrastructure by making investor-friendly policies. It has moved rapidly to enable foreign direct investment (FDI) in railways to increase infrastructure for freight and high-speed trains. At present, several domestic and foreign companies are also looking to invest in Indian rail projects.

Basic railway infrastructure includes the sub-grade, sub-ballast, ballast, sleepers (also known as crossties), rail, and track fastenings that secure the rail in position relative to the sleepers and to each other. These systems, the foundation for railway infrastructure, should be designed for the proposed purpose of the railway. Railways intended to carry heavy loads and require a solid sub-grade without underlying problems. Railways take advantage of the very low energy required to roll steel wheels over steel rails. But, because there is little friction between steel wheels and steel rail, railways must have low gradients gentle up and down slopes. Railway designers use many systems to minimize vertical grades. Designers use bridges and tunnels to traverse vertically challenging territory, cuts through rolling hills, and fills in low spots, often with material taken from cuts, to keep tracks as level as possible. They add drainage structures such as culverts concrete pipes or box-like structures that conduct water flows under the tracks and common ditches.

Trains are commonly heavy and the same thing that make them energy efficient. Each freight car and passenger carriage has air brakes at each wheel to slow and stop trains, but it still takes a lot of distance to stop a train often a kilometer or more. The higher the speed of the train, and the heavier the train, the longer it takes to bring it to a stop. Likewise, it takes a long time and distance to bring a heavy train out of a passing siding and up to track speed. These factors are considered in determining the value of “T” in the equation above. For single track lines with track speeds around 100 kph, with a modern signal system and using passing sidings (passing sidings can hold a typical train) a single track line can typically handle 30 trains a day at most (assuming half are in each direction). As the number of trains increases, interference between trains increases and delays to all trains on the line tend to get larger as well.

Railway engineers make great efforts to increase capacity, increase the speed of trains (this reduces T in the equation), build more sidings (also tending to reduce T), and modernize signal systems. As the number of train increases further, railways will connect passing sidings to provide piece of double track, permitting trains to pass while still moving and saving on the stopping and starting times. Finally, to create more capacity, the entire line will be double tracked. Capacity can also be an issue with double track lines. Trains can follow each other no closer than the stopping distance for the slowest train. In mixed freight, some trains may be slow either stopping at many small stations or very heavy, other trains may be fast. High speed differences between trains tend to limit line capacity even on double track, since trains have to switch tracks to get out of each other's way.

Some urban rail systems need as many as six tracks to allow the train frequencies needed in dense urban areas. Most busy railways install signals to control train movements. These are similar to road traffic lights and they allow trains to operate in both directions on single or multiple track railways. A single track signal systems may work only at the siding or station. Advanced signal systems have train presence detection and their indications are interlocked with switch positions to prevent trains from moving onto a track if there is oncoming traffic. 'Automatic block' is a common signal term for systems that are interlocked with the current siding and with sidings ahead and behind to prevent unsafe train movements.

Advanced signal systems rely on centralized systems to control a large territory. Highly advanced systems have computer controls that help dispatchers make sophisticated decisions about which trains to advance and which to delay. Modern signal systems are computerized train controls that require complex digital communication technology. These systems can impose control indications and stop trains automatically when they detect insecure conditions. High speed or very busy railways are often electrified. They use electric locomotives and draw electrical power, usually from overhead power distribution systems, but sometimes, in urban railways, via a third rail system at ground level. Major signal system components include signal boxes, display systems and the signal and communications cables needed to control these systems. Electrification system components include masts or poles, and a catenary system that delivers electrical current to the locomotive. Indian Railways is also looking for private partners to help modernise railway stations to world-class levels, and for projects focused on increasing connectivity with ports.

The high-density network connecting the four metropolitan cities of Chennai, Delhi, Kolkata and Mumbai, including its diagonals, popularly called the Golden Quadrilateral has got saturated at most of the locations. Given the present growth scenario, the Railways expect to carry 95 million tonnes incremental traffic per year and about 1,100 million tonnes revenue earning freight traffic by the end of the Eleventh Five Year Plan. This entails large investment for capacity augmentation.

Delhi Metro is equipped with the most modern communication and train control system introduced in the country for the first time. It is made according to international standard. Exceptional feature of Delhi Metro is its integration with other modes of public transport and a trendsetter for such systems in other cities of the country and in the South Asian region.

Problems in railway infrastructure:

- The quality of service provided leaves scope for substantial improvement in many areas.

- The average speed of trains is much lower than in other comparable countries.

- Railway safety is also an issue.

- The entire system is in urgent need of modernisation.

- The Rolling stock must be modernised and new.

- Higher capacity locomotives inducted.

- Average speeds must be significantly increased.

To summarize, India is ranked as fourth largest economy in the world. Nonetheless, India has the lack of adequate infrastructure. Physical infrastructure has immense impact on overall development of an economy. While strategies to quicken economic growth did anticipate the need for faster development of infrastructure as well. Several sectors such as electricity, railways, roads, ports, airports, irrigation, and urban and rural water supply and sanitation, continue to experience the pressure of rising demand for services even as they suffer from a considerable initial shortfall. Indian Railways is considered as second largest rail network around the globe under a single management, has been contributing to the development of the country’s industrial and economic land over a century. Of the two main segments of the Indian Railways, freight and passenger, the freight segment accounts for roughly two-thirds of revenues. Within the freight segment, bulk traffic accounts for nearly 95 percent, of which more than 44 percent is coal. Improved resource management, inter alia, through increased wagon load, faster turnaround time and a more rational pricing policy has led to an improvement in the performance of the railways.

Another infrastructure is port sector which is rapidly growing. It is a major driver of economy acceleration of nation. The goals of inclusive and high level of monetary growth can be accomplished if this infrastructure deficit is overcome. Infrastructure development also help to create a better investment environment in India. To develop infrastructure, there is a continuing need to re-examine the issues of budgetary allocation, tariff policy, fiscal incentives, private sector participation and public private partnerships to ensure that required infrastructure development takes place. The public sector plays a significant role in building transport infrastructure. Nonetheless, the resources needed are much larger than the public sector. It can provide public investment and to be supplemented by private sector investments, in Public Private Partnership mode. This strategy was followed in the Eleventh Plan and it has begun to show results. Public Private Partnerships are new phenomenon in India.