Inventory control

Inventory is the stock of any item or resource used in any company which include raw material, final products, component, parts, supplies, and work in process. Basically, "Inventory Control" focuses on the process of movement and accountability of inventory. This consists of strict policies and processes with reference to the physical and systemic movement of materials, Physical Inventory and cycle counting, Measurement of accuracy and tolerances and Good Accounting Practices. Management scholars defined Inventory Control as the supervision of supply, storage and accessibility of items in order to ensure an adequate supply without excessive oversupply.

The objective of inventory management is to have the appropriate amounts of materials in the right place, at the right time, and at low cost. An inventory management is an established process and controls that monitors level of inventory and determines what level should be maintained when stock is be replenished. Inventory control is needed to ensure that the business has the right goods to avoid stock-outs, to avoid shrinkage and to provide proper accounting. Inventory control encompasses the procurement, care and disposition of materials. Estimation of inventory is normally stated at original cost, market value, or existing replacement costs, whichever is lowest. This practice is done to lessen the possibility of overstating assets.

The perfect inventory and proper stock turnover will vary from one market to another. According to Barcodes Inc (2009), the inventory control system is a set of hardware and software based tools that automate the process of tracking inventory. The kinds of inventory tracked with an inventory control system can include almost any type of quantifiable good, including food, clothing, books, equipment, and any other item that consumers, retailers, or wholesalers may purchase.

The key step in inventory management is to gain correct information for inbound operations. The information so gained in advance can be a decisive factor in improving the inbound productivity.

There are three kinds of inventory that are of concern to managers which include raw materials, in-process or semi-finished goods, and finished goods. If a manager successfully controls these three types of inventory then capital can be released that may be tied up in unnecessary inventory, production control can be improved and can shield against obsolescence, deterioration and/or shoplifting. There are numerous reasons for inventory control such as it helps balance the stock as to value, size, colour, style, and price line in proportion to demand or sales trends, help plan the winners as well as move slow sellers, helps secure the best rate of stock turnover for each item, helps reduce expenses and markdowns, assists maintain a business repute for always having new, fresh merchandise in desired sizes and colours.

Inventory control systems range from eyeball systems to reserve stock systems to perpetual computer-run systems.

The Eyeball System: This is the standard inventory control system for the most of small retail and small manufacturing operations and is conveniently applied. The key manager stands in the middle of the store or manufacturing area and looks around. If they observe that some items are out of stock, they are reordered. In retailing, there are some difficulty with the eyeball as particularly good item may be out of stock for some time before anyone notices. If throughout the time it is out of stock then sales are being lost on it. Likewise, in a small manufacturing operation, low stocks of some particularly critical item may not be noticed until there are none left.

Reserve Stock System: This method involves keeping a reserve stock of items aside, often literally in a brown bag placed at the rear of the stock bin or storage area. I6 is more organized than eye ball system. When the last unit of open inventory is used, the brown bag of reserve stock is opened and the new supplies it contains are placed in the bin as open stock. At this time, a reorder is immediately placed. If the reserve stock quantity has been calculated correctly, the new delivery should arrive just as the last of the reserve stock is being used. In order to calculate the proper reserve stock quantity, it is necessary to know the rate of product usage and the order cycle delivery time. The differences on the reserve stock system only involve the management of the reserve stock itself.

Perpetual Inventory Systems: There are numerous kinds of perpetual inventory systems such as manual, card oriented, and computer- operated systems. In computer operated systems, a programmed instruction referred to commonly as a trigger, automatically transmits an order to the appropriate vendor once supplies fall below a prescribed level. The aim of each of the three types of perpetual inventory approaches are to register either the unit use or the dollar use of different items and product lines. This information help avoid stock-outs and to maintain a constant evaluation of the sales of different product lines to see where the emphasis should be placed for both selling and buying.

Inventory Control Records: Inventory control records are needed for buy-and-sell decisions. Some organizations control their stock by taking physical inventories at regular intervals, monthly or quarterly. Others use a dollar inventory record that gives an approximate idea of what the inventory may be from day to day in terms of dollars.

Perpetual inventory control records are useful for big-ticket items. Periodic physical counts are taken to validate the accurateness of the inventory card. Out-of-stock sheets, notify the buyer that it is time to reorder an item. Open-to-buy records help to avoid ordering more than is needed to meet demand or to stay within a budget. These records adjust order rate to the sales rate. Purchase order files keep track of what has been ordered and the status or expected receipt date of materials. Supplier files are valuable references on suppliers and can be very supportive in negotiating cost.

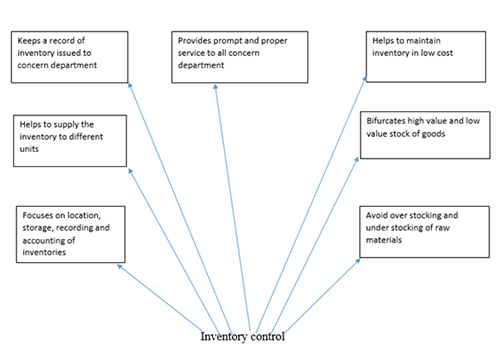

Inventory control is beneficial for organizations. Inventory control protects a company from fluctuations in demand of its products. It enables a company to provide better services to its customers. It keeps a smooth flow of raw-materials and aids in continuing production operations. It checks and maintains the right stock and reduces the risk of loss. It helps to lessen administrative workload, manpower requirement and even labour cost. It makes effective use of working capital by avoiding over-stocking. It helps to maintain a check on loss of materials due to carelessness or pilferage (stealing). It facilitates cost accounting activities. It avoids duplication in ordering of stock.

To summarize, an inventory control system is vital mechanism for companies to manage accounts, forecasting, replenishment, accounting services, and production planning. It refers to the process whereby the investment in materials and parts carried in stock is required within pre-determined unit set in accordance with inventory policy established by management.